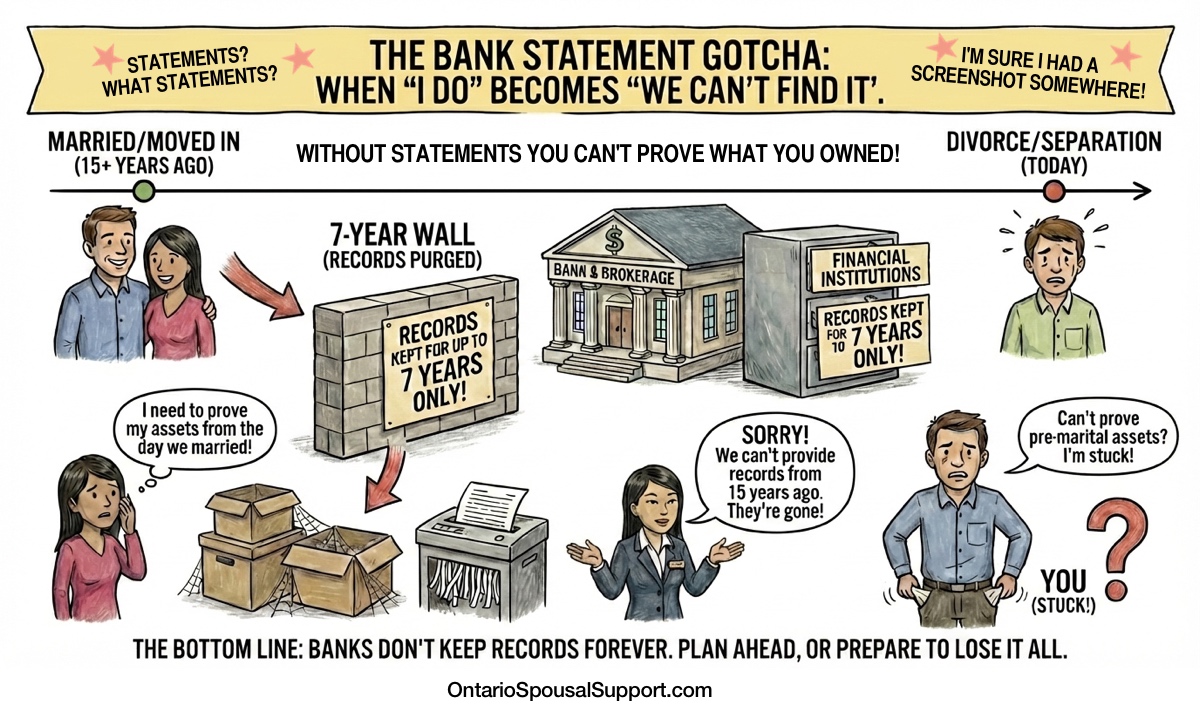

Banks and financial institutions in Canada keep records for 7-8 years, sometimes less. If you need to prove what you owned before you moved in together or got married, those records might already be gone.

Not misplaced. Not archived somewhere. Gone. Permanently deleted from their systems.

And if you can't prove what you brought into the relationship, the court might treat you as if you brought nothing.

The Financial Records Gotcha in 30 Seconds

The problem: Banks keep records for 7-8 years. Credit unions and brokers are similar or worse.

Why it matters: You need to prove what you owned at whichever came first—the date you moved in together OR the date you got married.

The math: Together 10+ years? Your records are almost certainly gone.

The consequence: Can't prove your pre-relationship assets? The court may assume you had none. Six-figure swings in property division.

The Problem Nobody Sees Coming

Sarah and Michael moved in together in 2006. Got married in 2009. Separating now in 2026.

Sarah had $85,000 in savings when they moved in together—money from selling a condo she owned before the relationship. That money went into their joint down payment on the house. Under Ontario family law, she should be able to exclude that $85,000 from property division. It was hers before the relationship started.

There's just one problem.

Her bank doesn't have records from 2006. They purged them years ago. The statements showing that $85,000 balance are gone. The wire transfer showing the condo sale proceeds? Gone. The paper trail proving she brought that money into the relationship? Doesn't exist anymore.

Now she's trying to prove a six-figure asset exclusion with no documentation. And Michael's lawyer is arguing she can't prove she had anything.

How Long Financial Institutions Actually Keep Records

Most people assume their bank keeps everything forever. They don't.

Major Canadian Banks (TD, RBC, BMO, Scotiabank, CIBC)

Retention period: 7-8 years typically

The big banks generally keep transaction records for seven years. Some stretch it to eight. After that, your statements, transaction histories, wire transfers, and deposit records get purged from their systems.

You can request statements for the past 7 years. Beyond that, you'll get a letter saying the records no longer exist.

They might keep basic account information longer—when you opened an account, when you closed it. But the detailed month-by-month statements showing your actual balances and transactions? Those are gone.

Credit Unions

Retention period: Varies (5-10 years)

Credit unions are all over the map. Some keep records for 10 years. Others purge at 5 years. There's no standard.

Smaller credit unions sometimes have worse record retention than big banks because they don't have the same storage infrastructure. I've seen credit unions that couldn't produce statements from 6 years ago.

Investment Brokers and Advisors

Retention period: 7 years (regulatory minimum)

IIROC (Investment Industry Regulatory Organization of Canada) requires investment dealers to keep records for seven years. Most stick to exactly that—seven years, not a day more.

This includes:

- Account statements

- Trade confirmations

- Portfolio valuations

- Account opening documents

After seven years, they're allowed to destroy them, and most do.

Insurance Companies

Retention period: 10+ years (but not always helpful)

Insurance companies tend to keep policy records longer than banks keep statements. They'll often have records going back 10-15 years or more.

The catch: they have records of your policies, not necessarily detailed financial statements. If you had a whole life policy with cash value, they might be able to reconstruct what the cash surrender value was on a specific date. But they won't have copies of every premium payment you made.

Mortgage Lenders

Retention period: 7 years after discharge

Mortgage lenders typically keep records for seven years after you pay off the mortgage. So if you had a mortgage you paid off in 2015, those records are probably gone by 2022.

This matters if you're trying to prove how much equity you had in a property you sold before the relationship, or if you're trying to reconstruct a down payment you made.

CRA (Canada Revenue Agency)

Retention period: Generally 10 years, sometimes longer

Here's the good news: CRA keeps records longer than banks do.

You can request copies of old tax returns going back 10 years, sometimes more. This won't give you bank statements, but it will show:

- Your income each year

- RRSP contributions (which suggests you had money to contribute)

- Investment income (which proves you had investments)

- Capital gains (which proves you sold assets)

Tax returns don't prove bank balances, but they're often the best alternative evidence you can get.

What You Actually Need to Prove

Under Ontario's Family Law Act, when you're dividing property, each person gets to exclude assets they brought into the relationship.

The critical date is whichever came first:

- The date you moved in together (cohabitation date), OR

- The date you got married

That date is your "valuation date" for what you owned going into the relationship.

You need to prove what your assets were worth on that exact date. Not approximately. Not "I remember having around $50,000." You need documentation.

What Counts as Pre-Relationship Assets

- Bank account balances

- Investment account values (RRSPs, TFSAs, non-registered accounts)

- Real estate equity (if you owned property before the relationship)

- Business ownership interests

- Pension values

- Cash value of life insurance policies

- Vehicles, jewelry, collectibles (if significant value)

For each of these, you need documentation showing the value on the date you moved in together or got married, whichever was earlier.

Why This Gets Messy Fast

Let's say you moved in together in 2004 and you're separating in 2026. That's 22 years ago.

No bank has records from 22 years ago. None.

Even if you moved in together in 2017 and you're separating in 2026, that's 9 years. Most banks have already purged those records.

The Brutal Math

Cohabitation date: 2015

Separation date: 2026

Years ago: 11 years

Bank retention: 7-8 years

Records available: None

And here's the part that makes people furious: the burden of proof is on you.

If you can't prove you had that $85,000 in savings, the court might assume you had zero. Your spouse's lawyer will absolutely argue you can't prove something you have no documentation for.

When This Becomes Critical

Long Marriages (10+ Years)

The longer you've been together, the more likely your records are gone.

If you've been together 15 years and you're separating now, your cohabitation date is 15 years ago. Way beyond any bank's retention period.

Grey Divorce (50+ Separating)

Grey divorce is exploding in Canada. People in their 50s, 60s, 70s who've been married 20, 30, 40 years.

These are exactly the people who likely had significant assets before marriage—inheritance money, proceeds from a previous home sale, savings from before the relationship.

And these are exactly the people whose records are completely gone.

Significant Pre-Relationship Assets

If you brought $10,000 into the relationship and you can't prove it, that's frustrating but probably not worth a legal fight over the difference.

If you brought $250,000 into the relationship and you can't prove it, you're talking about a six-figure swing in the property division. That's worth fighting about. And your spouse's lawyer knows it.

Second Marriages

Second marriages often involve people who already own property, have retirement savings, have pensions built up.

You meet someone at 45. You've been working for 20 years, you own a house, you have $200K in RRSPs. You move in together.

Ten years later you separate. You're 55. Your cohabitation date is 10 years ago. Your bank records are mostly gone.

But those pre-relationship assets you're trying to protect? They're the biggest part of what you own.

What You Can Use Instead of Bank Statements

If the bank records are gone, you need alternative documentation. Courts will accept other forms of proof, but it's harder to make the case.

Tax Returns

Request old tax returns from CRA. They show:

- Income (proves you had earnings to save)

- RRSP contributions (proves you had money to contribute)

- Investment income (proves you had investments generating returns)

- RRSP deduction limit (which is based on prior years' income)

Tax returns don't directly prove bank balances, but they paint a picture of your financial situation.

Investment Statements (If You Still Have Them)

If you printed and kept old RRSP or TFSA statements, those are gold.

Even if your brokerage won't provide old statements, if you personally saved paper copies or PDFs, those work.

Mortgage Documents

If you bought a house right before or right after moving in together, your mortgage application and closing documents will show:

- Down payment amount (where did that money come from?)

- Assets declared on the application

- Income at the time

Mortgage applications require you to list all your assets. If you declared $85,000 in savings on a mortgage app from around your cohabitation date, that's solid evidence.

Property Sale Records

If you sold a condo or house before moving in together, the closing documents show:

- Sale price

- Mortgage payout

- Net proceeds to you

You can get copies of old closing documents from your lawyer who handled the sale, the real estate brokerage, or from Land Registry records.

Employer Pension Statements

If you had a workplace pension, your employer or the pension administrator might have old statements showing your pension value on specific dates.

Pension statements often go back further than bank statements because pension administrators have different retention requirements.

Loan Applications

Any loan application (car loan, line of credit, personal loan) from around the time you moved in together will have required you to disclose your assets.

These applications are sometimes kept longer than bank statements.

Affidavits from Family Members

This is the weakest form of proof, but sometimes it's all you have.

If your parents can swear an affidavit saying "We gave Sarah $40,000 as a gift in 2005 which she deposited to her savings account," that's something.

It's not as good as a bank statement showing the deposit, but combined with other evidence (like your parents' bank statement showing they withdrew $40,000 that year), it can help.

Old Email or Documents

Did you email your parents about your finances back then? Forward a bank statement to someone? Mention your savings in an email when you were planning the house purchase?

Old emails can be powerful evidence if you still have them.

What Courts Will Accept

Ontario courts understand that old records disappear. They're not unreasonable about it.

But you need something. You can't just say "I had $85,000" with zero documentation.

Strong Evidence (Courts Love This)

- Actual bank statements from the date

- Investment account statements from the date

- Tax returns showing consistent high income (suggests savings)

- Property sale closing documents showing proceeds

- Mortgage application from around that time listing assets

Decent Evidence (Courts Will Consider)

- Tax returns combined with reasonable assumptions

- Pension statements

- Employment records showing income history

- Loan documents

- Affidavits from family combined with other evidence

Weak Evidence (Might Not Be Enough)

- Your own testimony with no documentation

- Affidavits from family with no corroboration

- Estimates based on "I remember"

The weaker your evidence, the more likely the court discounts your claimed assets or doesn't accept them at all.

Real Consequences

This isn't theoretical. The difference between proving your pre-relationship assets and not proving them can swing property division by six figures.

Example 1: The House Down Payment

You had $100,000 in savings when you moved in together. You put that toward the house down payment. Your partner put in $20,000.

House is now worth $900,000, mortgage is paid off.

If you can prove your $100,000: You exclude that from division. Your net family property is $400,000, your partner's is $440,000. They owe you $20,000 equalization.

If you can't prove it: The court treats the house as 50/50 from the start. Your net family property is $450,000 each. Nobody owes anybody anything.

Difference: $20,000. And that's a conservative example.

Example 2: Retirement Savings

You had $200,000 in RRSPs when you moved in together (second marriage, you were 45). Your partner had $50,000.

Now you're separating at 60. Your RRSPs are worth $600,000. Your partner's are worth $300,000.

If you can prove your starting $200,000: You exclude it. Your growth is $400,000, your partner's growth is $250,000. Equalization: they owe you $75,000.

If you can't prove it: The court might assume you both started at zero. Your RRSPs are $600,000, your partner's are $300,000. Equalization: you owe them $150,000.

Difference: $225,000. That's not a rounding error. That's retirement security.

What to Do Right Now

If Separation Is Possible (Even If Not Imminent)

Request your financial records today.

Call your bank and request statements for the past 7-8 years. Do this for every account:

- Chequing and savings accounts

- Credit cards

- Lines of credit

- Investment accounts

- RRSPs and TFSAs

Most banks will provide 7 years of statements for free or a small fee. Some charge per month ($5-$10 per statement). It might cost you $200-$300 to get everything.

That's nothing compared to losing the ability to prove a six-figure asset exclusion.

If You're Already Separated

Request records immediately, before more time passes.

If you separated 6 months ago and your cohabitation date was 7 years ago, you might still be within the window. Barely.

Request everything from every institution you've dealt with:

- Every bank you've had accounts with

- Every credit union

- Every investment brokerage

- Every pension administrator

- Every insurance company

If the Records Are Already Gone

Start gathering alternative documentation:

- Request old tax returns from CRA (10 years available)

- Contact old employers for pension statements

- Dig through old emails for any financial information

- Request old mortgage applications from lenders

- Get property sale documents from your old real estate lawyer

- Ask family members if they have any records (gifted money, loans, etc.)

- Check if you printed and saved any old statements

Build the strongest possible circumstantial case even if you don't have direct proof.

For Young Couples Just Starting Out

This advice sounds paranoid when you're 28 and just moving in together. I get it.

But do this anyway:

Try the Calculator

Want to see how property division and spousal support might work in your situation? Our calculators use the actual formulas Ontario courts rely on.

The calculator will show you estimated amounts and durations based on your inputs. It's a starting point—not a guarantee—but it's a lot better than guessing.

Frequently Asked Questions

How long do Canadian banks keep records?

Most Canadian banks keep records for 7-8 years. After that, statements, transaction histories, and account details are typically purged from their systems. Some may keep basic account information longer, but detailed transaction records are gone.

What date do I need to prove my assets from?

You need to prove what your assets were at whichever came first: the date you moved in together (cohabitation date) OR the date you got married. This is your "valuation date" for property division purposes.

What happens if I can't get my old bank statements?

You'll need alternative proof: old tax returns, employment records showing income, affidavits from family members who knew your financial situation, loan applications, mortgage documents, or any other documentation from that time period.

Can I use tax returns instead of bank statements?

Yes. CRA keeps records longer than banks (typically 10 years, sometimes more). You can request copies of old tax returns which show income, RRSP contributions, investment income, and other financial activity from the relevant time period.

Should I request my financial records now even if separation isn't imminent?

Yes. If there's any possibility of separation, request records now while they still exist. It costs nothing to ask, and you can't get them back once they're purged. This is especially critical if you've been together 5+ years.

Do credit unions keep records longer than banks?

Not necessarily. Credit unions vary widely—some keep records for 10 years, others purge at 5 years. There's no standard across credit unions, and smaller ones sometimes have worse retention than big banks.

What if my spouse had records but "lost" them?

If your spouse is claiming they had significant pre-relationship assets but conveniently can't prove it, the court will be skeptical. The burden is on them to provide documentation. No documentation usually means no exclusion.

Can I reconstruct my financial history from other sources?

Yes, but it's harder. Combine tax returns, employment records, pension statements, mortgage applications, and any other documentation you can find. Build a circumstantial case showing your financial situation at the time.

Does this apply to common-law relationships too?

Yes. Common-law spouses in Ontario face the same documentation challenges. Your cohabitation date is when you moved in together, and that's what you need to prove your assets from.

What if we kept separate finances the whole time?

Doesn't matter for property division. Under the Family Law Act, property division is based on net family property accumulated during the relationship, regardless of whose name things are in or whether you kept separate accounts.